What Is the Difference Between Apparel Sourcing and Garment Manufacturing?

February 18, 2026

Executive Summary

Bangladesh’s Ready-Made Garment (RMG) sector in 2026 bears little resemblance to the outdated perception of a low-cost, basics-only sourcing hub.

For UK, EU, and US brands, the competitive advantage of sourcing in Bangladesh is no longer defined solely by labor arbitrage. It is defined by systemic capability. The country & the clothing manufacturers in Bangladesh have undergone a structural transformation across industrial scale, safety governance, sustainability, and vertical integration.

The opportunity is real. The complexity is structural. Governance determines the outcome.

TL;DR — Key Takeaways for Sourcing Executives:

Beyond Basics: Bangladesh now manufactures complex outerwear, activewear, and engineered denim at scale.

Sustainability Leadership: The country hosts the highest number of LEED-certified green garment factories worldwide, signaling deep ESG maturity.

Vertical Integration: Local spinning, knitting, dyeing, and trim ecosystems drastically reduce dependency on imported raw materials and improve lead-time control.

Structural Cost Competitiveness: Efficiency-driven SMV (Standard Minute Value) optimization and scale dilution protect FOB margins, particularly for volume programs.

Favorable Trade Dynamics: Preferential market access for UK and EU brands materially improves Landed Duty Paid (LDP) calculations.

Infrastructure Upgrades: Port modernization and Matarbari deep-sea access are reducing historical congestion and improving logistics predictability.

The Governance Mandate: Risk is now governance-driven, not geography-driven. Direct-to-factory sourcing without structured oversight increases exposure to quality fade and compliance failures.

For decision-makers evaluating global sourcing allocation in 2026, the question is no longer whether Bangladesh is capable. The question is whether your sourcing governance is structured enough to fully leverage it.

Table of contents

ShowHide- The Evolution of Bangladesh’s RMG Sector: Beyond the Stereotypes

- Unmatched Scale and Production Capacity

- Cost Competitiveness in 2026: Why It Still Wins

- Labor Costs vs. Operator Efficiency

- Trade Structures and Landed Cost Dynamics Across the UK, EU and US

- The 2026 Cost Equation

- The Green Revolution: Leading the World in Sustainable Garment Sourcing & Manufacturing

- Infrastructure Upgrades and Shrinking Lead Times

- Strategic Implication for Global Buyers

- Navigating the Complexities: Why You Need a Sourcing Partner

- How a London-Based Sourcing Office Bridges the Gap

- The Strategic Conclusion

The Evolution of Bangladesh’s RMG Sector: Beyond the Stereotypes

For more than two decades, Bangladesh’s Ready-Made Garment (RMG) sector has been viewed through a narrow lens: low-cost, high-volume, basic apparel production. That perception is outdated.

In 2026, Bangladesh apparel sourcing represents a structurally evolved, compliance-driven, and technically capable manufacturing ecosystem that competes not only on price but increasingly on engineering capability, production scale, vertical integration, and governance discipline.

To understand why Bangladesh remains one of the strongest large volume garment sourcing destinations globally, decision-makers must separate legacy narratives from operational reality.

From Fast Fashion Basics to Value-Added Garments

Historically, Bangladesh built its export dominance on high-volume basics:

T-shirts

Polo shirts

Lightweight woven bottoms

Basic fleece

Entry-level knitwear

This specialization was not accidental. It was a strategic response to global fast-fashion demand in the 2000s and early 2010s. The country optimized for:

Labor-intensive production

Economies of scale

Lean manufacturing efficiencies

Aggressive FOB pricing

However, the past decade has seen a decisive shift.

By 2026, the competitive landscape has matured. Bangladesh is no longer just a “basics factory.” The industry has expanded significantly into value-added categories, including:

Technical outerwear

Performance and athleisure garments

Structured tailoring

Denim with advanced wash technologies

Seam-sealed and bonded products

Complex knit constructions

This transition was driven by three forces:

Buyer consolidation pressure: Global brands reduced supplier bases and demanded multi-category capability.

Margin compression in basics: Factories were forced to move up the value chain.

Capital reinvestment: Leading groups invested heavily in machinery, design capability, and vertical integration.

Today, major Bangladeshi manufacturing groups operate:

In-house fabric mills

Washing and finishing plants

Technical labs

Automated cutting systems

ERP-controlled production floors

The result is a shift from pure volume-driven production to engineering-led apparel manufacturing sourcing.

“Bangladesh is no longer competing solely on labor arbitrage. It is competing on production architecture and execution control.”

Buyers who still associate the country only with entry-level fast fashion are operating with an outdated sourcing thesis.

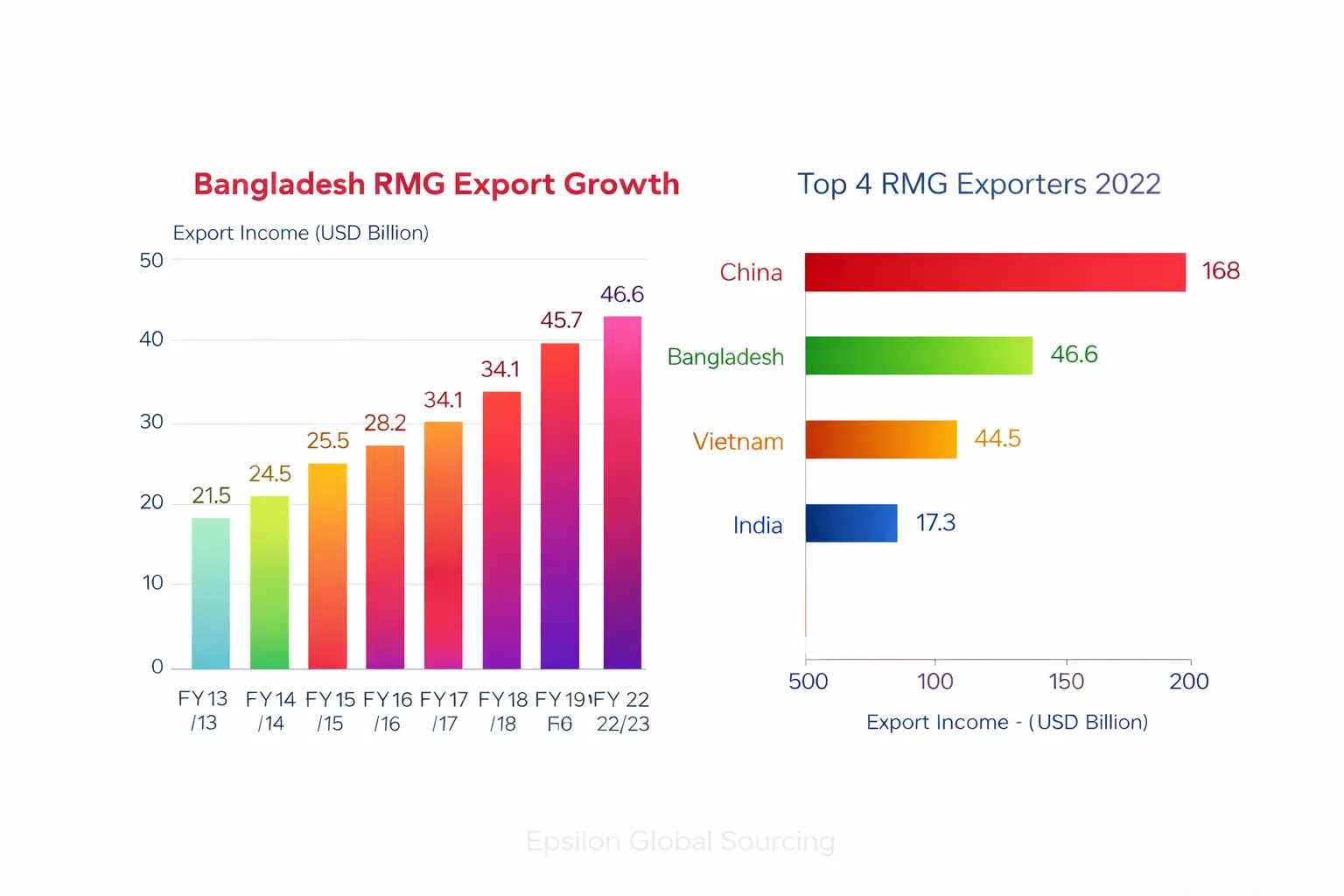

Data chart illustrating the rapid export growth and scale of the Bangladesh Ready-Made Garment (RMG) sector.

The Post-Rana Plaza Safety Revolution

No analysis of Bangladesh apparel manufacturing is credible without directly addressing the 2013 Rana Plaza collapse. It was a structural shock that reshaped the global sourcing industry.

The critical question for 2026 is not what happened in 2013.

The real question is: What changed afterward?

The answer is significant.

Following the tragedy, two unprecedented compliance initiatives were implemented:

Accord on Fire and Building Safety in Bangladesh

Alliance for Bangladesh Worker Safety

These programs introduced:

Mandatory structural inspections

Fire safety remediation requirements

Electrical safety upgrades

Transparent reporting mechanisms

Strict corrective action timelines

Thousands of factories underwent structural, fire, and electrical audits. Non-compliant units were suspended or permanently closed. Billions of dollars were invested in remediation.

The result is an uncomfortable but factual reality:

Bangladesh is now one of the most heavily audited apparel sourcing destinations in the world.

In many cases, factory compliance visibility in Bangladesh exceeds that of:

Emerging African sourcing hubs

Smaller South Asian competitors

Certain Southeast Asian clusters

This transformation also changed buyer behavior. Today, global brands operating in Bangladesh typically require:

SMETA audits

BSCI compliance

Structural certifications

Third-party fire approvals

Digital production transparency

The compliance infrastructure has become institutionalized rather than reactive.

“The post-2013 regulatory architecture did not simply repair buildings. It rebuilt the governance model of the industry.”

For sourcing executives, this matters.

Risk mitigation is no longer optional. It is embedded into the ecosystem.

In summary, the evolution of Bangladesh’s RMG sector is not cosmetic. It is structural. The country has transitioned from a volume-centric basics hub to a compliance-intensive, increasingly technical, and globally integrated manufacturing platform.

The stereotype has expired.

The opportunity, however, has not.

Contact us to discuss apparel sourcing requirements in Bangladesh.

Our team provides factory matching, costing transparency, compliance oversight, and end to end production management.

Unmatched Scale and Production Capacity

For any serious sourcing executive, one question overrides all marketing narratives:

Can they handle my volume without operational instability?

In 2026, Bangladesh’s answer is unequivocal.

The country is not merely a manufacturing location. It is a mass-scale production ecosystem engineered for industrial output at a level that few sourcing destinations can replicate. Scale is not incidental. It is structural.

Bangladesh’s RMG sector now operates as a dense industrial cluster with:

Thousands of export-oriented factories

Concentrated labor pools with category specialization

Embedded compliance infrastructure

Mature port logistics through Chattogram and inland depots

Institutionalized buyer coordination systems

The implication for brands is straightforward:

"Bangladesh is one of the very few countries capable of absorbing large-volume apparel programs while maintaining price competitiveness and delivery predictability."

The Core Strengths: Denim, Cotton, and Knitwear

Bangladesh’s global dominance is not evenly distributed across all categories. It is strongest where industrial depth meets technical repetition.

1. Denim

Bangladesh has become one of the world’s largest exporters of denim garments. The sector benefits from:

Industrial-scale washing plants

Advanced laser and ozone finishing technologies

Sustainable water-reduction processes

High-capacity cutting and stitching lines

Major international brands rely on Bangladesh for:

Core five-pocket denim

Stretch denim programs

Fashion washes

Mid-range premium positioning

The country’s advantage lies in its ability to produce denim at scale while managing wash complexity and cost efficiency.

2. Cotton-Based Apparel

Bangladesh’s specialization in cotton garments is historically rooted but technologically upgraded.

Strength factors include:

Skilled workforce in cotton knits and woven bottoms

High-efficiency sewing lines optimized for repetition

Deep supplier familiarity with global cotton sourcing patterns

For buyers running large cotton-based programs such as:

T-shirts

Polo shirts

Sweatshirts

Basic woven trousers

Bangladesh remains one of the most commercially viable sourcing platforms in the world.

3. Knitwear Dominance

Bangladesh’s knitwear cluster is particularly formidable.

The ecosystem includes:

Circular knitting mills

Rib and collar producers

Dyeing and finishing plants

Printing and embroidery facilities

This concentration allows for:

Faster fabric replenishment

Reduced MOQ constraints

Strong cost engineering

High-volume repeat programs

“When evaluating sourcing destinations, category specialization matters more than headline export figures. Bangladesh’s knit and denim clusters are industrially mature, not experimental.”

The Rise of Vertical Integration

Historically, one criticism of Bangladesh sourcing was dependence on imported raw materials, particularly from China. Lead times were therefore partially exposed to upstream supply chain volatility.

That dynamic has materially shifted.

Over the past decade, Bangladesh has invested heavily in vertical integration, particularly in:

Local spinning mills

Knitting mills

Dyeing and finishing plants

Trim and accessories production

The objective has been clear:

Reduce reliance on imported raw materials and compress total lead time.

The results are visible in three areas.

1. Lead Time Compression

For cotton knit programs, factories can now source:

Yarn locally

Fabric domestically

Trims within the country

This reduces:

Import dependency delays

Customs exposure

Transit buffer requirements

In practical terms, this allows for:

Faster repeat orders

More agile in-season replenishment

Reduced working capital tied up in pipeline inventory

2. Cost Stability

Local sourcing of yarn and trims reduces:

Currency fluctuation exposure

Freight volatility

External geopolitical dependency

This creates stronger cost predictability for FOB programs.

3. Greater Production Control

Vertical integration also improves:

Fabric quality monitoring

Shade consistency

Batch traceability

Production planning synchronization

When fabric and garment production operate within aligned ownership groups, execution discipline improves.

“Vertical integration does not eliminate supply chain risk. It redistributes control. In Bangladesh’s case, it has shifted meaningful control back inside the domestic ecosystem.”

In summary, Bangladesh’s scale is not theoretical. It is operational.

Its strength in denim, cotton, and knitwear, combined with expanding vertical integration, positions it as one of the few sourcing destinations capable of absorbing serious volume while maintaining commercial competitiveness.

For brands asking whether Bangladesh can handle large programs, the more relevant question in 2026 is:

Can your sourcing governance handle Bangladesh’s scale effectively?

Contact us to discuss apparel sourcing requirements in Bangladesh.

Our team provides factory matching, costing transparency, compliance oversight, and end to end production management.

Cost Competitiveness in 2026: Why It Still Wins

Cost remains the dominant variable in global apparel sourcing decisions. Procurement teams benchmark FOB. CFOs model landed margins. Boards assess sourcing shifts through the lens of geopolitical exposure and total cost architecture.

The persistent question in 2026 is direct:

Is Bangladesh still cost competitive, or has the wage gap closed?

The answer requires nuance.

Bangladesh does not win purely because labor is inexpensive. It wins because of a structural combination of:

Labor architecture

Operator productivity

Scale-driven overhead dilution

Vertical integration

Trade positioning

Total Landed Duty Paid (LDP) dynamics

Buyers who evaluate only headline wage rates misunderstand the sourcing equation.

Labor Costs vs. Operator Efficiency

For years, Bangladesh was labeled a “low-wage sourcing hub.” That framing is strategically incomplete.

While wage levels remain competitive relative to many Asian peers, cost advantage in 2026 is less about wage arithmetic and more about Standard Minute Value (SMV) optimization.

Modern Bangladeshi factories increasingly operate with:

Automated cutting systems

Real-time production tracking platforms

Dedicated industrial engineering departments

Lean production specialists

Precision line balancing

The outcome is measurable:

Higher operator output per hour

Reduced idle time

Lower rework ratios

Improved line efficiency percentages

In practical terms, even where nominal wages increase, the cost per garment unit remains competitive because productivity per operator improves.

“Sourcing cost is a function of efficiency, not wage level.”

Skilled operators in mature Bangladeshi clusters demonstrate high repetition speed and stability in:

Knitwear programs

High-volume denim lines

Structured woven basics

Factory groups investing in automation also achieve:

Improved marker efficiency

Reduced fabric wastage

Lower defect ratios

More predictable SMV calculations

These factors reduce hidden cost drivers that erode FOB competitiveness elsewhere.

Trade Structures and Landed Cost Dynamics Across the UK, EU and US

Beyond factory-level economics, Bangladesh’s most powerful competitive lever lies in trade architecture.

UK and EU Markets

Bangladesh benefits from preferential market access into Europe.

Access to the European market has historically been facilitated under the European Union Generalised Scheme of Preferences framework.

Following Brexit, Bangladesh continues to benefit from preferential access into the UK under the UK Generalised Scheme of Preferences implemented by the Government of the United Kingdom.

The financial implications are material.

Duty-free or reduced-duty treatment results in:

Lower import tariffs into EU and UK markets

Improved gross margins

Enhanced landed cost predictability

For buyers calculating Landed Duty Paid (LDP) cost, the equation includes:

FOB price

Freight

Insurance

Customs clearance

Import duties

Where duty is zero or materially reduced, Bangladesh’s competitive position strengthens immediately.

In comparison, sourcing from countries without preferential access can add:

8 to 12 percent duty exposure in certain categories

Direct margin compression

Retail price pressure

“The sourcing decision is not made at FOB. It is made at LDP.”

For high-street and price-sensitive segments in Europe, a few percentage points in duty differential can determine category viability.

The US Landed Cost Equation

The United States operates under a different tariff framework. Bangladesh does not benefit from broad preferential access into the US in the same manner as in the EU or UK.

This alters the duty structure, but it does not eliminate competitiveness.

For US brands, landed cost must account for:

FOB price

Ocean freight

Insurance

Import duties

Inland US logistics

Even where duties apply, Bangladesh frequently remains competitive due to:

Structurally efficient FOB pricing

Scale-driven overhead dilution

SMV-optimized production

Vertical integration reducing upstream volatility

In high-volume categories such as:

Cotton knit basics

Core denim

Entry-level woven bottoms

Bangladesh continues to serve as a margin-efficient production base for US brands.

“For US buyers, Bangladesh’s advantage lies less in tariff arbitrage and more in scale efficiency and cost engineering.”

While nearshore sourcing may serve ultra-fast replenishment cycles, Bangladesh remains commercially rational for volume-driven seasonal programs.

The 2026 Cost Equation

Bangladesh wins on cost not because it is universally the cheapest, but because it integrates:

Competitive labor architecture

Increasing operator productivity

Scaled industrial output

Vertical integration

Preferential access in Europe

Scale-driven margin efficiency for US programs

When evaluated at the Landed Duty Paid level, Bangladesh remains one of the most financially efficient sourcing destinations for UK and EU brands and continues to deliver commercially compelling economics for US volume categories.

Cost competitiveness in 2026 is not accidental. It is the result of layered structural advantages developed over decades.

For brands seeking margin protection in volatile retail environments across London, Berlin, or New York, Bangladesh remains a strategically rational anchor within a diversified global sourcing portfolio.

Contact us to discuss apparel sourcing requirements in Bangladesh.

Our team provides factory matching, costing transparency, compliance oversight, and end to end production management.

The Green Revolution: Leading the World in Sustainable Garment Sourcing & Manufacturing

If cost and scale answer the procurement question, sustainability answers the boardroom question.

In 2026, ESG performance is no longer a marketing narrative. It is embedded into:

Retailer risk assessments

Investor scrutiny

Regulatory compliance frameworks

Consumer brand positioning

For global fashion brands, sourcing decisions are now evaluated not only by margin contribution but by environmental footprint, social governance, and supply chain transparency.

Bangladesh’s transformation in this domain is one of the most underappreciated shifts in global apparel manufacturing.

The Highest Number of LEED-Certified Factories Globally

Bangladesh currently holds the highest number of LEED-certified garment factories in the world, certified under the U.S. Green Building Council framework.

U.S. Green Building Council administers the globally recognized LEED standard. Certification requires measurable compliance across:

Energy efficiency

Water conservation

Indoor environmental quality

Sustainable material use

Waste reduction

Bangladesh does not merely participate in LEED certification. It leads it.

The country hosts:

Dozens of Platinum-rated facilities

Numerous Gold-rated factories

Large-scale green industrial complexes purpose-built for sustainability

This development is strategic, not cosmetic.

Leading Bangladeshi manufacturing groups have invested in:

Solar energy installations

Natural daylight optimization in factory floors

Rainwater harvesting systems

Low-energy dyeing machinery

Advanced insulation and ventilation systems

The financial logic is compelling:

Lower long-term operating costs

Reduced energy dependency

Stronger positioning with ESG-focused buyers

Improved workforce retention through better working environments

“In sustainability benchmarking, Bangladesh is no longer catching up. In green-certified garment factories, it is setting the pace.”

For brands under pressure from investors and regulators, sourcing from LEED-certified facilities provides measurable ESG reporting leverage.

Exterior of a LEED-certified green garment factory in Dhaka, Bangladesh, featuring solar panels and sustainable architecture.

Water Treatment (ETP) and Circular Fashion Initiatives

Environmental risk in apparel manufacturing is most visible in water usage and chemical discharge.

Bangladesh’s regulatory and industry evolution has focused heavily on:

Effluent Treatment Plants (ETPs)

Wastewater recycling

Zero liquid discharge processes

Chemical management systems

Modern dyeing and washing facilities in Bangladesh increasingly operate with:

In-house ETP systems

Real-time water monitoring

Sludge management controls

Compliance with international wastewater discharge standards

Factories that previously discharged untreated wastewater are no longer part of compliant export supply chains.

This shift is reinforced by buyer audit regimes and international compliance programs.

amfori and Sedex frameworks further strengthen environmental governance through structured auditing.

Circular Materials and Recycled Inputs

Bangladesh is also scaling capability in:

Recycled polyester (rPET) production

Organic cotton sourcing

Regenerated fiber blends

Waste fabric recycling initiatives

Vertical integration has enabled garment groups to:

Incorporate recycled yarn into knit programs

Develop certified organic cotton collections

Offer traceability documentation

Reduce raw material waste

Global fashion brands are increasingly allocating sustainable capsule collections to Bangladesh due to:

Cost-effective recycled fiber production

Availability of certified mills

Alignment with ESG disclosure requirements

“Circular fashion is no longer experimental in Bangladesh. It is commercially deployable at scale.”

Strategic Implication for 2026

Bangladesh’s sustainability leadership is not accidental. It emerged from:

Post-crisis compliance restructuring

Buyer-driven audit intensity

Capital reinvestment by major factory groups

Regulatory alignment with global environmental standards

For brands operating in ESG-sensitive markets such as the UK and EU, Bangladesh offers:

Measurable green building credentials

Structured water treatment systems

Scalable circular production

Governance transparency

In 2026, sustainability is not a secondary consideration in apparel sourcing. It is a primary screening variable.

Bangladesh has positioned itself not as a low-cost polluter, but as a scaled, ESG-aligned manufacturing ecosystem capable of meeting the environmental expectations of modern global fashion brands.

Contact us to discuss apparel sourcing requirements in Bangladesh.

Our team provides factory matching, costing transparency, compliance oversight, and end to end production management.

Infrastructure Upgrades and Shrinking Lead Times

If cost is predictable and compliance is controlled, the final sourcing variable is time.

For UK, EU, and US buyers alike, logistics risk can outweigh production risk. Late shipments trigger:

Retail markdown exposure

Missed promotional windows

Air freight escalation

Working capital distortion

Inventory imbalance across distribution centers

Historically, Bangladesh faced criticism around port congestion and shipment delays. In 2026, that narrative requires reassessment.

The country has invested aggressively in port modernization, inland connectivity, and deep-sea access, materially improving export reliability for both transatlantic and transpacific routes.

Port Innovations and Deep Sea Access

Bangladesh’s primary export gateway is the Port of Chittagong, now widely referred to as Chattogram Port.

Over the past decade, the port has undergone structural upgrades including:

Expanded container handling capacity

Modernized terminal equipment

Improved digital customs clearance systems

Increased yard optimization

Extended operational throughput efficiency

Container performance has strengthened through:

Reduced dwell times

Streamlined customs digitization

Expanded use of private inland container depots supporting pre-clearance

The second structural shift lies in the development of the Matarbari Deep Sea Port.

Matarbari is strategically significant because it:

Enables handling of larger mother vessels

Reduces reliance on feeder transshipment via Singapore or Colombo

Shortens maritime transit cycles

Lowers congestion dependency

For UK and EU buyers, this translates into:

Improved sailing frequency

Greater vessel schedule predictability

Reduced production planning buffers

For US buyers, the implications are equally important:

More stable East Coast and West Coast routing

Improved container allocation reliability

Reduced exposure to cascading feeder delays

“Lead time is no longer purely a factory variable. It is an infrastructure variable. Bangladesh has begun addressing both.”

In parallel, road connectivity between major industrial clusters such as Gazipur and Narayanganj and the port corridors has improved, reducing inland transit volatility before export departure.

Cargo containers and shipping cranes at Chittagong Port, handling global apparel exports from Bangladesh.

Realistic Production Calendars for UK, EU & US Brands

Infrastructure improvements are only relevant if they translate into realistic delivery timelines.

In 2026, for established, compliant factories with confirmed fabric availability, a practical production calendar appears as follows.

Sample Timeline: 60 to 90 Days from PO to Shipment

Day 0–7: Order Confirmation & Pre-Production

Purchase Order issuance

Tech pack finalization

Fabric booking confirmation

Trim approvals

Day 10–30: Fabric Production

Yarn sourcing or allocation

Knitting or weaving

Dyeing and finishing

Lab dips and bulk shade approval

Day 30–60: Garment Manufacturing

Cutting

Sewing

Inline quality control

Finishing and packing

Day 60–75: Final Inspection & Port Movement

AQL inspection

Carton consolidation

Inland transfer to port

Day 75–90: Vessel Departure

Container loading

Export clearance

Shipment departure

Transit Profiles by Region

UK & EU

Transit time to major European ports typically ranges between:

18 to 30 days depending on routing

Shorter where direct services are available

For repeat programs with pre-booked fabric, production can compress closer to:

45 to 60 production days

United States

For US buyers, the total sourcing calendar must incorporate longer sea transit.

Typical ocean freight ranges:

East Coast ports such as New York or Savannah: 28 to 40 days

West Coast ports such as Los Angeles or Long Beach: 32 to 45 days depending on routing

A realistic PO-to-US-port arrival cycle generally falls within:

90 to 120 days total

For replenishment programs with committed fabric and stable capacity:

60 to 75 days ex-factory

30 to 40 days transit

“The difference between a 60-day and 90-day production cycle is rarely factory incompetence. It is planning discipline.”

“For US buyers, Bangladesh is not primarily a speed strategy. It is a scale and margin strategy.”

Contact us to discuss apparel sourcing requirements in Bangladesh.

Our team provides factory matching, costing transparency, compliance oversight, and end to end production management.

Navigating the Complexities: Why You Need a Sourcing Partner

Bangladesh in 2026 offers scale, cost competitiveness, sustainability leadership, and modernizing infrastructure.

However, sourcing success is not determined by geography alone.

It is determined by governance architecture.

The difference between a profitable sourcing program and a margin-eroding one rarely lies in factory capability. It lies in:

Supplier selection discipline

Production control systems

Contract enforceability

Real-time problem resolution

Cross-border coordination maturity

The strategic error many UK, EU, and US brands make is assuming that strong factories eliminate sourcing risk.

They do not.

They reduce production risk. Commercial and operational risk remain.

Bangladesh rewards structured sourcing strategies.

It penalizes transactional ones.

The Hidden Costs of Direct-to-Factory Sourcing

On paper, direct sourcing appears rational. Remove the intermediary. Negotiate sharper FOB. Communicate directly with the factory.

In practice, this frequently creates an Iceberg Cost Structure.

Visible Cost:

Lower quoted FOB

Hidden Costs Below the Surface:

Communication delays

Misinterpreted tech packs

Quality fade across bulk production

Unapproved subcontracting

Rework and air freight escalation

Compliance exposure

Cultural and time-zone misalignment

Import documentation risk for US buyers

“The FOB price is visible. Execution risk is not.”

1. Communication Delays

Time-zone separation between Bangladesh and Western markets introduces structural friction.

For UK and EU brands, misalignment can create 24-hour response cycles.

For US brands, particularly West Coast teams, the gap can extend further.

This affects:

Sample correction cycles

Fabric shade approvals

Label compliance queries

Packaging confirmations

Import documentation clarification

Small delays compound into production drift.

2. Unapproved Subcontracting

During peak season capacity pressure, factories may outsource portions of production without explicit buyer visibility.

Without on-ground monitoring, brands risk:

Social compliance violations

Inconsistent workmanship

Audit exposure

US customs scrutiny under stricter import enforcement frameworks

Subcontracting risk is not theoretical. It is structural when oversight is weak.

3. Quality Fade

Quality fade occurs when:

Initial samples are carefully supervised

Bulk production oversight weakens

Inline supervision becomes reactive rather than preventive

The outcome:

Higher defect ratios

Carton-level rejections

Increased returns in retail markets

Margin erosion

Attempting to save 2 to 3 percent at FOB can create 8 to 12 percent margin loss at retail.

This is equally true for:

UK high-street brands

EU multi-brand distributors

US department store suppliers

An Epsilon GS apparel sourcing agent conducting a rigorous quality control inspection inside a Bangladesh manufacturing facility.

How a London-Based Sourcing Office Bridges the Gap

A sophisticated sourcing partner does not replace the factory.

It governs the interface between brand and manufacturer.

For UK, EU, and US brands, a London-headquartered sourcing office with operational presence in Dhaka creates structural advantages.

1. UK-Enforceable Commercial Framework

Contracts governed under UK jurisdiction provide:

Clear dispute resolution pathways

Structured commercial accountability

Reduced contractual ambiguity

Defined liability parameters

For US brands, this also offers:

Western commercial alignment

Transparent financial governance

Legal clarity beyond purely offshore agreements

This creates buyer-side confidence that purely direct offshore arrangements cannot replicate.

2. On-Ground Teams in Dhaka

Effective sourcing requires physical presence.

An integrated model includes:

Dedicated QC inspectors in Dhaka

Inline production monitoring

Pre-shipment AQL inspections

Real-time escalation to factory leadership

This eliminates blind spots between:

Approved samples

Inline bulk output

Final shipment readiness

“Sourcing without physical oversight is delegation without control.”

For US buyers operating across multiple time zones, this local presence prevents problems from escalating overnight.

3. Real-Time Cross-Atlantic Problem Solving

Time-zone lag is operational risk.

A London-based commercial office aligned with Western business hours ensures:

Immediate response to buyer concerns

Rapid commercial clarification

Faster approval loops

Escalation without 24-hour delay cycles

Simultaneously, Bangladesh-based teams manage:

Factory floor execution

Compliance verification

Capacity constraints

Corrective action implementation

For US brands, this dual-layer structure provides:

Western-facing commercial coordination

Local production control

Reduced import documentation errors

Stronger oversight of labeling and regulatory compliance

The communication gap collapses.

4. Supplier Governance and Selection Discipline

The greatest risk in Bangladesh is not the country.

It is supplier misalignment.

An experienced sourcing partner:

Pre-screens factory groups

Audits technical capability beyond marketing claims

Evaluates vertical integration depth

Assesses real capacity versus declared capacity

Monitors subcontracting exposure

Reviews ESG compliance consistency

This governance layer protects:

UK brands from reputational exposure

EU brands from regulatory non-compliance

US brands from import enforcement and customs risk

The Strategic Conclusion

Bangladesh in 2026 is one of the most structurally competitive apparel sourcing destinations in the world.

Its advantages are no longer limited to labor cost. They now include:

Industrial scale

Category specialization

Vertical integration

Sustainability leadership

Infrastructure modernization

However, structural strength does not guarantee commercial outcomes.

Without disciplined governance, brands expose themselves to:

Margin erosion

Compliance exposure

Production volatility

Reputational risk

With structured sourcing architecture, including Western commercial oversight, on-ground execution control, and intelligent supplier governance, Bangladesh shifts from being merely cost-effective to being strategically resilient.

The critical mistake in modern sourcing strategy is binary thinking.

It is not Bangladesh versus nearshore.

It is not cost versus speed.

It is not scale versus compliance.

It is portfolio design.

For brands serving London, Berlin, or New York, Bangladesh functions best as a margin-anchoring, volume-capable production base within a globally diversified sourcing framework.

The opportunity is real.

The complexity is permanent.

The competitive advantage belongs to brands that combine scale access with professional sourcing governance.

Frequently Asked Questions About Sourcing from Bangladesh

If your brand is seeking a reliable apparel sourcing partner with access to Tier 1 and mid-tier factories in Bangladesh, Epsilon Global Sourcing provides:

- End to end apparel sourcing service

- Factory capability matching

- Transparent costing breakdown

- Compliance and audit oversight

- Multi stage quality control

- LC and documentation handling

- Production tracking and reporting

Contact us to discuss your sourcing needs and strengthen your supply chain with a high performing Bangladesh apparel sourcing team.

{kind=link}

{kind=link}

{kind=link}